By Ajai Chaudhary | AI Innovation, AI Trends

Nobody planned this.

There was no climate summit that decided AI would become the catalyst for the clean energy transition.

There was no policy paper. No government mandate. No industry roadmap. And yet, something remarkable is quietly happening.

The same technology being criticised for its insatiable appetite for electricity is — almost by accident — doing what decades of energy policy struggled to achieve.

It is accelerating the global transition to clean energy faster than anyone expected.

The Scale of AI’s Power Problem

Let us start with the numbers, because they are hard to ignore.

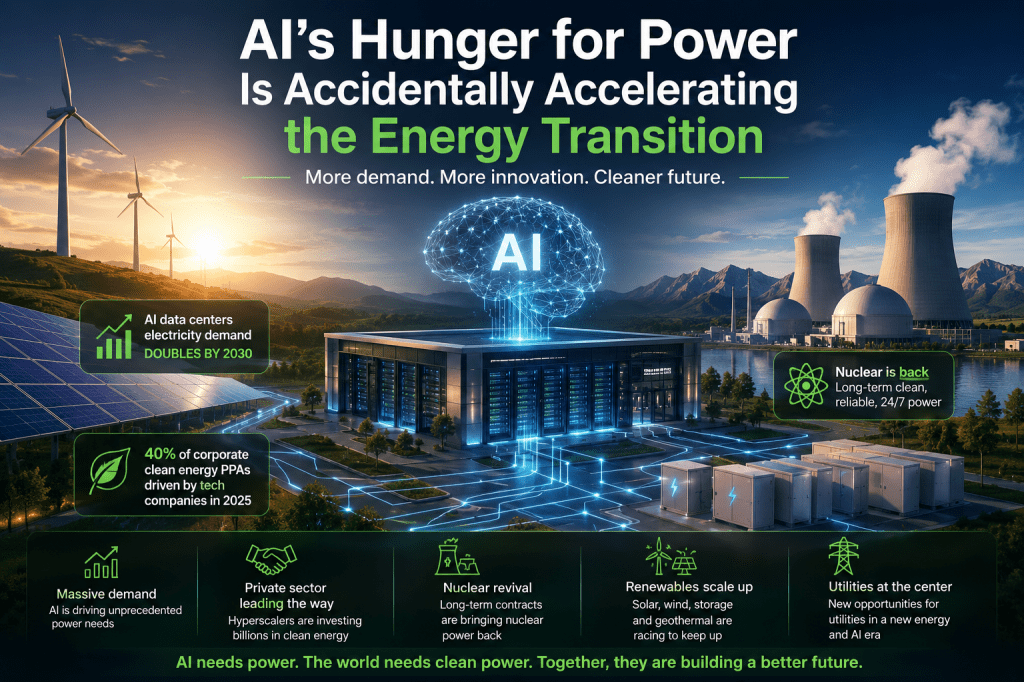

According to the International Energy Agency, electricity demand from data centres surged by 17% in 2025 alone — well outpacing global electricity demand growth of 3%.

AI-focused data centres grew even faster.

Looking ahead, total data centre electricity consumption is set to double by 2030, with power use from AI-focused facilities set to triple.

That is not incremental growth.

That is a structural shift in global energy demand.

And behind those numbers is something equally striking.

The capital expenditure of just five large technology companies — Microsoft, Amazon, Google, Meta, and others — surpassed $400 billion in 2025. That figure is set to increase by a further 75% in 2026.

When capital flows at this scale, it does not just create demand.

It reshapes entire industries.

The Uncomfortable Irony

Here is where the story gets interesting.

The same organisations driving this demand surge are also under enormous pressure — from shareholders, regulators, and their own sustainability pledges — to power their operations with clean energy.

That combination of massive demand and clean energy obligation is creating something nobody anticipated.

A private-sector clean energy investment wave unlike anything seen before.

In 2025, Amazon, Meta, Google, and Microsoft collectively accounted for nearly 49% of all global clean power purchase agreement (PPA) volumes.

To put that in context: four technology companies are now driving almost half of the world’s corporate clean energy procurement.

That is not an energy transition nudged by policy.

That is an energy transition being pulled forward by data centres.

The Nuclear Moment Nobody Expected

Perhaps the most striking consequence of AI’s energy hunger is the revival of nuclear power.

For years, nuclear was a technology in managed decline.

High costs. Ageing plants. Public scepticism. Limited investment.

Then the hyperscalers arrived.

Nuclear offers something renewables alone cannot: firm, dispatchable, carbon-free baseload power, available around the clock, regardless of weather or season.

For data centres that cannot afford intermittency, that is not just attractive. It is essential.

The deals that have followed represent a genuine inflection point.

Microsoft signed a landmark 20-year, 837 MW Power Purchase Agreement with Constellation Energy to restart a decommissioned nuclear plant — a deal that would have seemed unthinkable just a few years ago.

Amazon expanded its nuclear offtake agreement with Talen Energy to 1,920 MW through 2042 — one of the largest corporate nuclear procurement deals in history.

Google signed the largest corporate nuclear PPA ever recorded — a deal with Kairos Power for Small Modular Reactors (SMRs) expected to come online in the early 2030s.

Meta partnered with Oklo to develop a 1.2 GW power campus using 16 Aurora Powerhouse reactors, with first reactors expected operational by 2030.

And Amazon has led a $500 million financing round in X-energy to develop gas-cooled SMRs — targeting at least 5 GW of new nuclear capacity by 2039.

This is not a niche movement.

This is the private sector writing cheques that regulators and governments could not.

Renewables Are Racing to Keep Up

Nuclear is only part of the story.

Renewables remain the fastest-growing energy source for data centres, with total generation increasing at an annual average rate of 22% between 2024 and 2030.

By the end of this decade, renewables are expected to meet nearly 50% of the growth in data centre electricity demand.

The mechanism here is straightforward.

Technology companies have aggressive net-zero commitments.

They need clean power at unprecedented scale.

And the fastest way to procure it is through long-term renewable energy contracts.

The result: data centres accounted for around 40% of all corporate renewable PPAs signed in 2025.

Solar farms. Wind projects. Battery storage. Advanced geothermal.

All being developed and financed — at least in part — because a hyperscale operator needed clean electrons at scale.

This Is Not the Clean Energy Transition Anyone Designed

The traditional story of the energy transition was built around policy.

Carbon pricing.

Renewable portfolio standards.

Government subsidies.

International climate agreements.

Those levers matter. But they move slowly.

What AI’s demand surge is demonstrating is that market pull can move faster than policy push.

When technology companies need 1,920 megawatts of nuclear power, they do not wait for a policy framework.

They sign a 20-year contract and write the cheque.

When four companies account for half of global corporate clean energy procurement, they are not responding to a regulation.

They are responding to their own operational requirements — and their own sustainability commitments.

The energy transition is still happening.

It is just being accelerated by an unlikely catalyst.

What This Means for Utilities and Energy Leaders

For utilities and energy companies, the implications are significant.

1. New Categories of Energy Customer Are Emerging

Hyperscale operators are not typical commercial or industrial customers.

They require:

- firm, reliable capacity at scale

- long-term contractual certainty

- high renewable content

- increasingly, nuclear or advanced clean energy options

- significant transmission infrastructure

Understanding and serving this customer segment requires a different capability set than traditional utility operations.

2. Grid Infrastructure Is Becoming a Competitive Constraint

One of the least-discussed consequences of AI’s energy demand is the pressure now building on transmission infrastructure.

Grid connection timelines in many markets are already stretching to years, not months.

Transmission bottlenecks are limiting where data centres can locate.

New infrastructure investment decisions that once took decades are now being compressed.

Utilities that can offer reliable grid connection, transmission capacity, and long-term power certainty will have a structural advantage in attracting this investment.

3. Clean Energy Capability Is No Longer Optional

The technology sector’s clean energy expectations are reshaping what it means to be an energy supplier.

A utility that cannot offer credible renewable or nuclear sourcing will find itself increasingly excluded from hyperscale energy procurement processes.

This is not a future consideration.

It is already playing out in energy markets today.

4. The Investment Signal Is Clear

Global data centre electricity is projected to grow from 460 TWh in 2024 to 1,300 TWh by 2035.

That is nearly three times today’s demand in just over a decade.

For utilities, energy developers, and infrastructure investors, the signal could not be clearer:

The demand is coming. The question is who will be positioned to serve it cleanly.

The Strategic Question

For energy executives, this raises a fundamental strategic question.

Is our organisation positioned to benefit from AI’s clean energy pull — or are we watching from the sidelines?

Because the capital is already flowing.

The technology companies are already building.

The nuclear contracts are already signed.

The renewable PPAs are already in place.

The energy transition is no longer waiting for a policy window.

It is being driven by data centre demand, corporate sustainability commitments, and private capital at a scale that policy alone could never mobilise.

The organisations that recognise this shift — and position themselves to serve it — will find themselves at the centre of one of the most significant infrastructure investment cycles of this decade.

A Final Thought

There is a neat irony at the heart of this story.

AI — the technology being blamed for rising data centre emissions — is simultaneously becoming one of the most powerful catalysts for the clean energy transition in a generation.

Not through design.

Not through regulation.

But through the simple logic of appetite meeting obligation.

AI needs power at massive scale.

The companies building AI have committed to clean power.

And the combination of that demand and that commitment is moving capital, reviving nuclear, building renewables, and forcing grid modernisation faster than any climate summit managed.

This is not the clean energy story anyone wrote.

But it may be one of the most consequential ones playing out right now.

Leave a comment